Navigating Roof Insurance Claims: What Chicago Homeowners Need to Know

- 25min

- Published:10/1/2025

- ByShaunak Ahuja

Imagine waking up to water dripping from your ceiling after a severe Midwest thunderstorm, or discovering missing shingles following those notorious Chicago winter winds. These moments unleash a flood of stress and uncertainty about what comes next. Don’t worry, we’re here to help.

As roof replacement experts with decades of experience in the Chicago area, our team at HX Home Solutions has created this guide to provide straightforward, actionable information for Greater Chicago residents facing roof issues. Let us help you understand when your insurance will (and won't) cover roof replacement.

When Does Homeowners Insurance Cover Roof Replacement?

Whether your homeowners insurance will cover roof replacement costs depends on several key factors: the cause of damage, your roof's age, and the specific terms outlined in your policy. If your roof only needs minor repairs, insurance companies often prefer this less expensive option rather than approving a total roof replacement.

Illinois insurers often apply stricter scrutiny to roof claims than other home insurance claims because of our region's weather patterns. They may send specialized adjusters who are trained to distinguish between storm damage and normal aging, particularly in older Chicago suburbs where houses are usually older.

Note: Most insurance companies reduce coverage for roofs over 20 years old, and many won't cover roofs over 30 years old, regardless of their condition and material.

How to Get Your Roof Claim Approved: Step-by-Step Guide

Properly documenting and filing your roof claim can dramatically increase your chances of approval. In Illinois, most insurance companies require claims to be filed within 30-60 days of the damage occurring, though some may give you up to one year for certain types of damage. Follow these steps to get your claim approved.

1. Document the Damage Immediately

Take date-stamped photos and videos of all visible damage from multiple angles, including interior water damage if present. Focus on capturing clear images of missing or damaged shingles, dented gutters, and any debris that could have caused impact damage.

Expert tip: Create a detailed inventory of all damaged areas, noting their specific locations on your roof (north side, above garage, etc.) to help your adjuster locate them easily.

2. Review Your Policy Coverage and Deductible

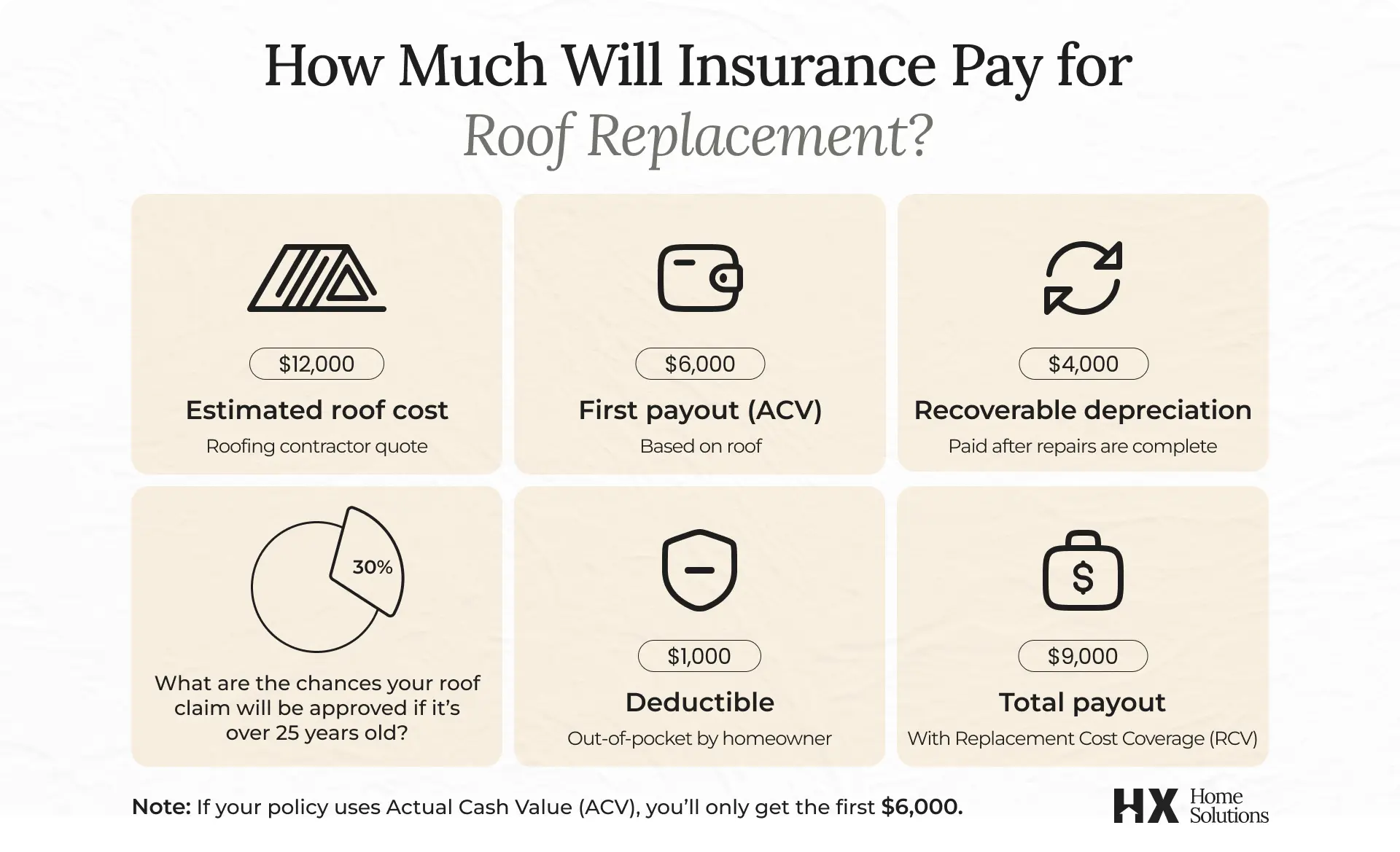

Carefully read your policy to understand your coverage type, deductible amount, and any exclusions that might apply. Pay special attention to whether you have Actual Cash Value (ACV) or Replacement Cost Value (RCV) coverage, as this significantly impacts your payout.

Expert tip: If you have a separate wind/hail deductible (common in Illinois policies), note that it's often higher than your standard deductible.

3. Contact a Reputable Local Contractor for Inspection

Schedule an inspection with a licensed roofing contractor with experience with insurance claims in the Chicago area. Illinois requires roofing contractors to be licensed and insured, so verify these credentials before you hire anyone.

4. File Your Claim Promptly

Contact your insurance company to initiate your claim, providing the date of the damage and a brief description of what happened. In Illinois, you generally have 1-2 years to file a claim, but many policies require notification within 30-60 days of the damage occurring. The sooner you can file the claim, the better.

5. Meet with the Insurance Adjuster

Be present during the insurance adjuster's inspection and point out all damaged areas you've documented. If possible, your contractor should also be present during this inspection to professionally address any technical questions or disputes.

6. Get Multiple Repair/Replacement Estimates

Ideally, you’ll get detailed written estimates from 2-3 reputable contractors. In the Chicago area, roof replacement typically costs between $5,000-$15,000 for average-sized homes, depending on materials and complexity.

7. Review the Insurance Settlement Offer Carefully

Compare the insurance company's settlement offer with your contractor estimates, noting any discrepancies in the scope of work or material quality. Pay attention to any depreciation holdbacks that you may be able to recover after completing the work.

Expert tip: Don't cash the initial check if it includes language stating that accepting payment constitutes a "full and final settlement" when you believe the amount is insufficient.

If your claim is denied or the offered amount seems insufficient, don’t get discouraged. You have the right to appeal. Illinois law provides strong consumer protections for insurance disputes, including the option to file a complaint with the Illinois Department of Insurance.

What to Do If Your Claim Gets Denied

Receiving a claim denial can be frustrating, but it doesn't have to be the final word. Many successful roof replacements began with initial denials that were later overturned through proper appeals and documentation.

- Contact your insurance agent: Speak directly with your agent to understand exactly why your claim was denied and what options you have for reconsideration. Request the specific policy language that was used to justify the denial.

- Collect evidence: Gather additional documentation to support your case, including contractor assessments, weather reports confirming storm activity in your area, and photos documenting the damage timeline. Consider hiring a public adjuster for an independent assessment.

- Appeal the decision: Submit a formal written appeal to your insurance company, including all supporting documentation and a clear explanation of why you believe the claim should be covered. In Illinois, insurance companies must respond to appeals within specific timeframes.

- File a complaint: If your appeal is unsuccessful, you can file a complaint with the Illinois Department of Insurance, which provides consumer protection services and can intervene in disputed claims.

- Take legal action: As a last resort, consult with an attorney specializing in insurance claims. Illinois law provides several legal protections for policyholders that an experienced attorney can leverage on your behalf.

Don’t be afraid to be persistent; it often pays off in insurance appeals. Many claims are initially denied simply because of insufficient documentation or misunderstandings about policy coverage.

Working with Contractors on Insurance Roof Replacements

You have the right to choose your roofing contractor for a roof replacement covered by your home insurance, even if your insurance company has a preferred vendor list. Your policy pays for the approved repairs, regardless of which qualified contractor performs the work.

Local contractors familiar with Chicago building codes and insurance requirements can make a significant difference in your roof replacement experience. They understand common issues with local housing styles and have relationships with area suppliers and inspectors.

Here’s what to look for in a Chicago-area roofing contractor:

- Proper licensing and insurance: Verify the contractor has current Illinois roofing licenses and liability insurance, and workers' compensation coverage. This protects you from liability if accidents occur during your roof replacement.

- Local experience and reputation: Choose contractors with an established presence in the Chicago area and verifiable references from local homeowners. Experienced local contractors understand our unique weather challenges and building code requirements.

- Insurance claims expertise: Select a contractor with specific experience handling insurance claims and the documentation they require. The right contractor can help interpret adjuster reports and ensure all covered damage is properly addressed.

- Detailed, written estimates: Professional contractors provide comprehensive written estimates that include material specifications, labor costs, timeline expectations, and warranty information. This documentation is essential for insurance claims.

Think of a reputable roofing contractor as your advocate throughout the insurance claims process, helping document damage, providing detailed estimates, and sometimes communicating directly with adjusters to explain technical aspects of necessary repairs.

They can help you appeal denied claims by providing expert assessments of damage and explanations of why repairs are needed according to industry standards and building codes.

Your Roof, Protected by Experts

By knowing what's covered, documenting damage properly, and working with reputable professionals, you can navigate the insurance claim process and protect your home.

HX Home Solutions has been the trusted exterior remodeling company for Chicago homeowners for over 70 years. We have an A+ rating and Accreditation with the Better Business Bureau, alongside other accolades.

Our experienced team provides free roof inspections, thorough documentation for insurance claims, and expert installation using premium materials. Contact us today for assistance with your roof insurance claim or replacement needs.

.avif)