When Insurance Will (and Won't) Cover Your Home's Siding Damage in Chicago

- 35min

- Published:7/1/2025

- ByShaunak Ahuja

According to the NOAA storm events database, in 2024 alone, Cook County experienced 215 registered storm events, including tornadoes, thunderstorm winds, and damaging hail. For many homeowners, discovering siding damage after these events leads to an immediate question: Will my insurance cover siding?

The short answer is yes, homeowners insurance typically covers siding damage, but it depends on several factors. As siding replacement experts serving the Chicago area for over 75 years, HX Home Solutions has guided countless homeowners through this process and understands the complexities of insurance claims for exterior damage.

When Homeowners Insurance Typically Covers Siding Damage

Homeowners insurance policies typically cover sudden, accidental damage to your home's siding, as opposed to deterioration from normal wear. Most standard HO-3 home insurance policies include dwelling insurance coverage that extends to siding, though important conditions and coverage limits apply that you should understand.

The biggest problem with insurance is that it usually covers repairs only, and it can be stressful to prove the need to replace siding altogether. This often results in unmatched design or colors that affect your home's appearance. Remember that your coverage ultimately depends on your specific policy type, which brings us to an important distinction.

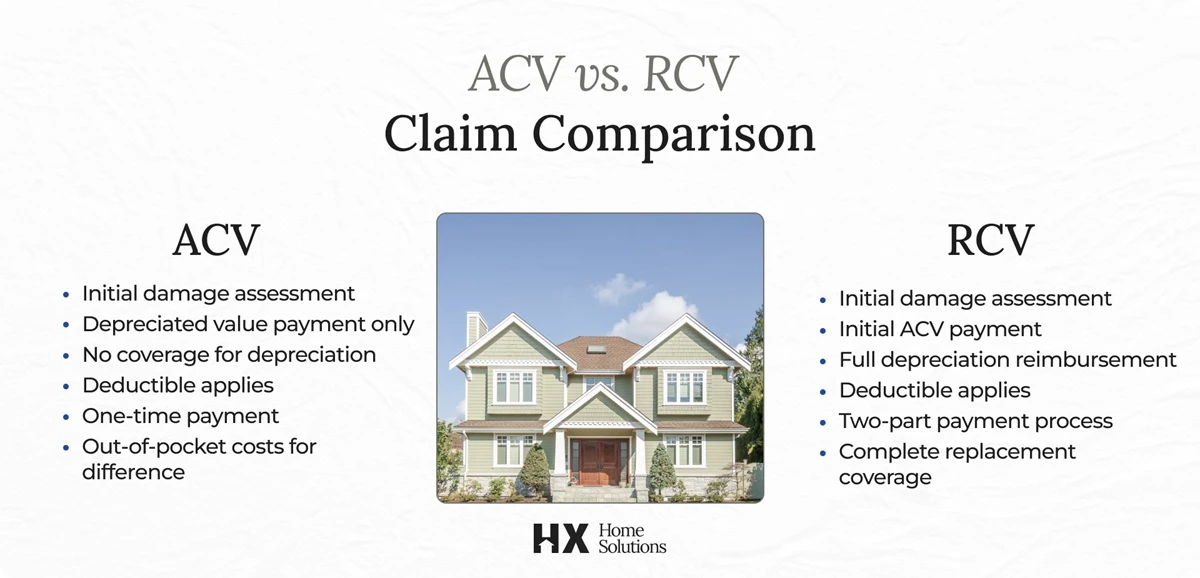

Understanding Your Policy Type: ACV vs. RCV

The difference between Actual Cash Value (ACV) and Replacement Cost Value (RCV) policies can dramatically impact your out-of-pocket expenses.

With an ACV policy, you'll receive the depreciated value of your damaged siding. For example, if your 10-year-old vinyl siding is damaged by hail, and it had a 20-year expected lifespan, your insurance company might pay only 50 percent of the replacement cost, minus your deductible.

RCV policies, although they have a more expensive premium, provide significantly better insurance coverage. With an RCV policy, you'll initially receive the ACV payment, but after completing siding repair, you can submit receipts to receive the rest of the replacement amount. This often makes RCV policies worth the extra cost for homeowners concerned about potential siding damage from common perils.

Insurance adjusters factor typical siding lifespans when calculating depreciation, so knowing your siding's expected durability helps you understand potential claim outcomes.

Steps to Successfully File a Siding Damage Claim

Our team knows firsthand that navigating the insurance claim process can be overwhelming, especially when you're already dealing with damaged areas. We’ve outlined a structured approach that will help ensure you receive the maximum coverage your insurance policy allows. Here's how to proceed with your siding claim:

1. Document Everything Immediately

Take extensive photos and videos of all damaged areas before making any temporary repairs. Capture close-ups of the damage and wider shots showing entire walls. This documentation is crucial if your insurance company questions the extent of the siding damage later.

2. Contact Your Insurance Company Promptly

Don’t delay contacting your insurance. Most homeowners insurance policies require notification within a specific timeframe, typically 48–72 hours after discovering the damage. Delayed reporting could jeopardize your claim. When calling, have your insurance policy number ready and ask about your coverage limits, deductible amount, and next steps.

3. Understand Your Policy Coverage and Deductible

Review your policy documents carefully before the adjuster's visit. Pay special attention to coverage limits, exclusions, and whether you have ACV or RCV coverage. These details allow more informed conversations with your adjuster and prevent surprises during the claim process.

4. Meet with the Insurance Adjuster

Be present during the adjuster's inspection and point out all damaged areas. Don't hesitate to show your documentation if the adjuster misses anything. Remember that adjusters usually handle multiple claims daily and might not notice all the damage without your guidance.

5. Get a Professional Assessment

Having a reputable local contractor evaluate the damage offers valuable support for your claim. Experienced contractors familiar with storm damage can identify issues adjusters might miss and provide detailed repair estimates that help justify replacement rather than repair.

6. Review the Settlement Offer Carefully

Compare the insurance company’s offer against your contractor's estimate. Ensure it reflects all repair needs, and check if any depreciation holdbacks will be released upon completion (common with RCV). If your siding project involves replacing undamaged siding, confirm whether this will be reimbursed or considered cosmetic.

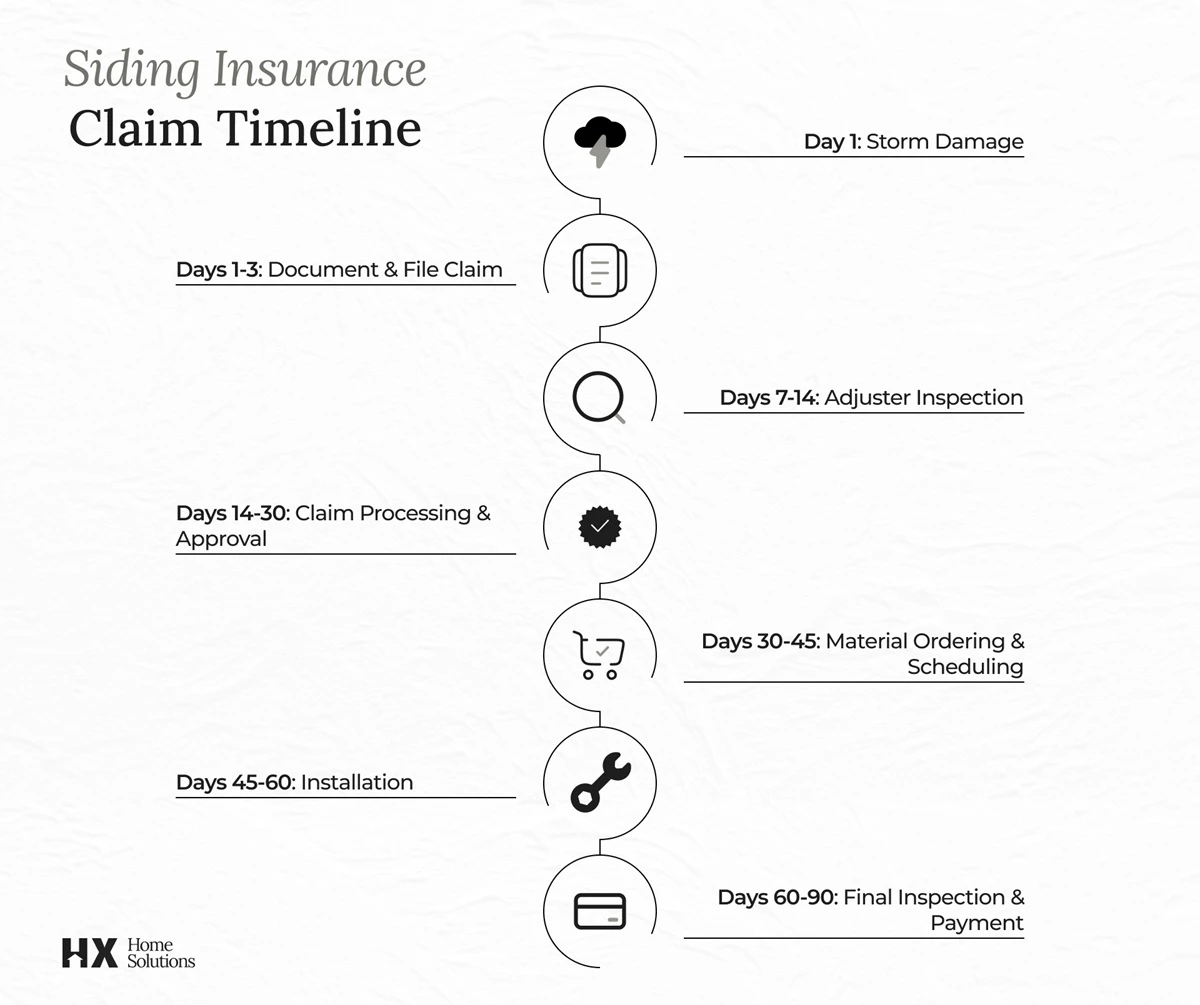

How Long Does Insurance Siding Repair Take?

The timeline for insurance coverage for siding repairs or replacement varies a lot. From the moment you file a claim to completing installation, it may take 1–3 months. Once your claim is approved, most siding contractors can install new siding within 1–2 weeks, weather permitting. However, insurance claim processing, material ordering (especially for aluminum siding or vinyl siding), and scheduling may delay the siding replacement timeline.

What to Do If Your Claim Is Denied

Receiving a claim denial can be frustrating, but don’t give up; it doesn't mean you're out of options. Insurance companies may deny claims for various legitimate reasons, but sometimes these decisions warrant a second look.

Common reasons for siding claim denials in Illinois include:

- Policy exclusions (maintenance vs. sudden damage)

- Missed filing deadlines

- Insufficient documentation

- Disagreements about the cause of damage (particularly with wind claims)

- Pre-existing damage

- Cosmetic damage only (no functional impairment)

Building Your Appeal Case

To successfully challenge a claim denial, gather comprehensive evidence supporting your position. Here's what to collect:

- Written denial explanation from your insurance company

- Independent contractor assessments and damage reports

- Additional photos and video documentation

- Weather reports from the date of damage

- Statements from neighbors with similar damage

- Expert opinions on whether the damage is cosmetic or functional

Take these practical next steps:

- Request a detailed explanation in writing

- Review your policy carefully for coverage details

- Get an independent professional assessment

- Consider appealing the decision through your insurer's process

- Understand your options with the Illinois Department of Insurance for unfair claim practices

Remember that persistence often pays off. Many initially denied claims get approved upon appeal when homeowners present compelling evidence and professional assessments.

Avoid Surprises with Our Experienced Team

Understanding your homeowners insurance coverage for siding damage before you need to file a claim is the best way to avoid surprises and disappointment. The differences between policy types, covered perils, and claim processes can significantly impact your out-of-pocket expenses and the final appearance of your home. While there are many moving parts to consider, this isn’t something you need to go through alone.

At HX Home Solutions, our professional house exterior remodeling team has decades of experience in siding installation and replacement throughout Chicago. We also help homeowners navigate the often confusing insurance claim process, from initial documentation to final installation. We strive to build relationships with our customers, helping them for years.

Contact us today for a free inspection and expert guidance on your siding damage situation. We're here to help you restore your home's protection and appearance with minimal stress.

.avif)